- May 7, 2026

- Tech

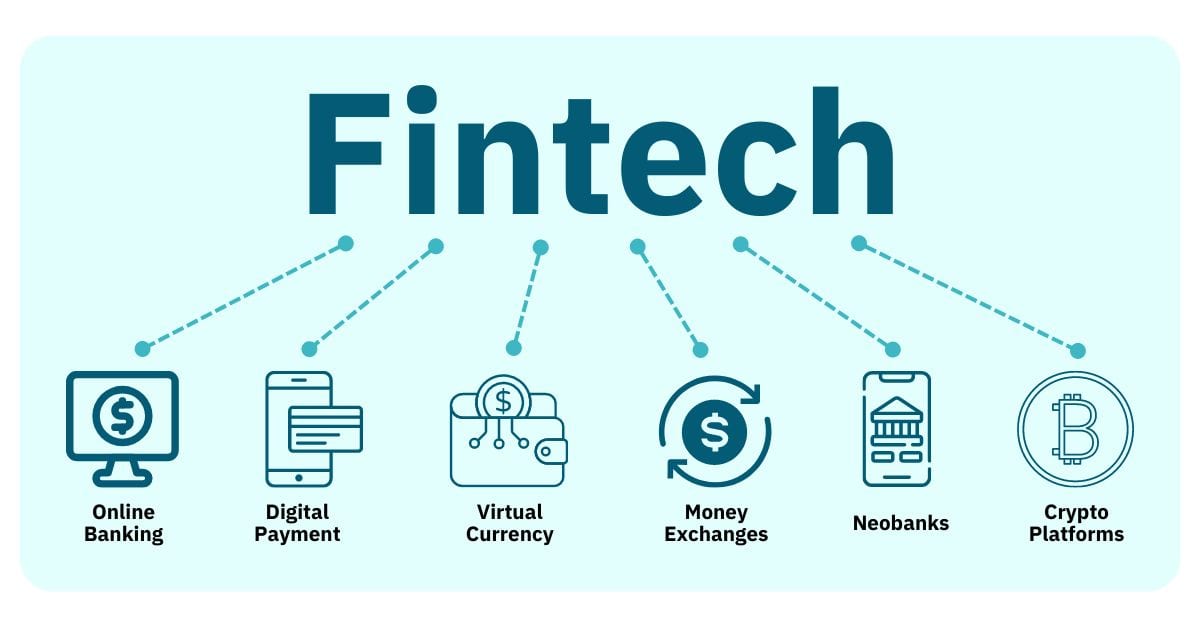

Fintech: A continuing evolution

Fintech, or financial technology, refers to the innovative application of technology to improve and automate financial services. While the term "fintech" gained prominence in the 21st century, its roots trace back much further, evolving through distinct phases.

Here's an overview of Fintech's evolution:

I. Early Foundations (Fintech 1.0: Late 19th Century - 1967)

This era laid the groundwork for digitized financial services, focusing on infrastructure development.

Telegraph and Transatlantic Cables (Late 19th Century): Revolutionized the speed of financial information transfer across borders.

Fedwire Funds Service (1918): Established by the Federal Reserve Banks, this was an early electronic funds transfer system using telegraph lines.

Credit Cards (1950s): Diner's Club, American Express, and BankAmericard (Visa) transformed consumer spending and credit.

ATMs (1967): Barclays introduced the world's first ATM, offering 24/7 cash access and pioneering self-service banking.

II. Digital Revolution (Fintech 2.0: 1967 - 2008)

This period saw a significant shift from analog to digital finance, driven by increasing computerization and the internet.

Inter-bank Computer Bureau (1968) & ACH (US): Paved the way for automated clearing houses, facilitating electronic funds transfers between banks.

NASDAQ (1971): The world's first digital stock exchange, revolutionizing securities trading.

SWIFT (1973): Standardized and secured communication for international money and security transfers.

Online Banking (1980s): Enabled limited account management from home, changing how people interacted with financial institutions.

Early AI for Fraud Detection (1990s): AI systems like FinCEN Artificial Intelligence (FAIS) began reviewing transactions to flag potential money laundering.

PayPal (1998): Hinted at the new payment systems that would emerge with the rise of the internet.

III. Post-Crisis Disruption and Digital Transformation (Fintech 3.0: 2008 - Present)

The 2008 financial crisis, coupled with rapid technological advancements (especially smartphones), spurred a new wave of innovation and disruption.

Loss of Trust in Traditional Banks: Created an opening for new, agile startups.

Smartphone Adoption and Internet Connectivity: Enabled mobile banking, peer-to-peer lending, and digital wallets to flourish.

Bitcoin and Blockchain (2009 onwards): Introduced decentralized digital currencies and a secure, transparent ledger technology.

Rise of Fintech Startups: Companies like Wealthfront (robo-advisors), Square (mobile payments), Kickstarter (crowdfunding), and Transferwise (P2P money transfer) emerged, challenging traditional models.

Open Banking and APIs: Regulations and technologies allowing third-party access to financial data, fostering collaboration and new product development (e.g., India's UPI).

Robo-advisors: Automated, algorithm-driven investment advice, making investing more accessible and affordable.

Payment Innovations: Widespread adoption of digital wallets (Apple Pay, Google Pay), QR code systems, and real-time payment networks like FedNow.

Embedded Finance: Integration of financial services directly into non-financial platforms (e.g., "Buy Now, Pay Later" options on e-commerce sites).

Neobanks (Digital-Only Banks): Offer competitive rates, low fees, and seamless digital experiences by eliminating physical branches.

Regtech: Use of technology to automate and streamline regulatory compliance, helping financial firms meet complex rules.

Insurtech: Applying technology to simplify and streamline the insurance industry.

IV. The Future of Fintech: Emerging Trends

The evolution continues with a focus on deeper integration of advanced technologies and a more customer-centric approach.

AI and Machine Learning (AI/ML):

Hyper-personalization: Tailoring financial products and services based on vast amounts of customer data.

Enhanced Fraud Detection: AI algorithms analyzing real-time transaction data to identify anomalies.

Automated Finance Management: AI-driven applications for investment portfolio management, loan evaluations, and savings plans.

Conversational Banking: AI chatbots and virtual assistants providing 24/7 customer support.

Algorithmic Fairness: Addressing bias in AI for critical financial decisions like credit approval.

Blockchain and Decentralized Finance (DeFi): Beyond cryptocurrencies, blockchain is being explored for secure data storage, smart contracts, and more efficient cross-border payments. DeFi aims to create financial services without traditional intermediaries.

Embedded Finance Expansion: Further seamless integration of financial services into everyday non-financial activities.

Open Banking and Banking-as-a-Service (BaaS): Continued collaboration between traditional banks and fintechs, enabling banks to offer their infrastructure to external providers.

Cybersecurity and Biometric Authentication: Increased focus on robust security measures like fingerprint and facial recognition to protect sensitive financial data.

Central Bank Digital Currencies (CBDCs): Many countries are exploring digital versions of their national currencies.

Green Fintech/Sustainability: Growing emphasis on environmentally friendly financial products and services, and ESG (Environmental, Social, and Governance) data intelligence.

Fintech's evolution is a continuous journey driven by technological innovation, changing consumer demands, and the need for greater efficiency, accessibility, and personalization in financial services. It is transforming how individuals and businesses manage their money, creating a dynamic and increasingly interconnected financial ecosystem.